Land Subsidence in the UK: Why Your Property Could Be Sinking and How to Know Before It’s Too Late

If you own a home in London or the Southeast—particularly a Victorian or Edwardian property—there’s something happening beneath your foundations that you probably can’t see. And by the time you do see it, the damage may already be done.

Land subsidence in the UK has cost the economy an estimated £3 billion over the past decade. Last year alone, insurers handled 45,000 domestic subsidence claims. And with climate change bringing hotter, drier summers, experts predict the problem will only get worse.

But here’s what most homeowners don’t realise: subsidence doesn’t announce itself with dramatic cracks overnight. The ground shifts gradually—millimetres at a time—long before any visible signs appear. By the time your doors start sticking or cracks snake across your walls, you’re already dealing with a problem that could cost tens of thousands to fix and knock up to 20% off your property’s value.

The good news? Technology now exists that can detect these tiny ground movements from space, giving you advance warning months or even years before damage becomes visible. The same satellite monitoring used by the British Geological Survey and major insurers is now available to individual property owners.

This guide explains everything you need to know: what causes subsidence in British properties, which homes are most at risk, what it really costs, and how you can protect your investment before the next heatwave hits.

The UK’s £3 Billion Ground Problem

Subsidence is the downward movement of the ground beneath a building, causing foundations to shift and structures to crack. It’s different from settlement—the normal, uniform sinking that happens shortly after construction—and from heave, which is upward movement when soil swells.

What makes subsidence particularly damaging is that it’s uneven. One corner of your house sinks while another stays put, creating the diagonal cracks and structural distortion that surveyors dread.

The numbers tell a stark story. The British Geological Survey classifies shrink-swell clay movement as the most damaging geohazard in Britain today. Insurance claims spike dramatically after hot, dry summers: the 2018 heatwave alone triggered over 10,000 claims worth £64 million in just three months—the highest quarterly jump in more than 25 years of records.

And it’s getting worse. In the first half of 2025, following the UK’s warmest spring on record, insurers paid out £153 million across roughly 9,000 households. The average claim now stands at £17,264—and that figure keeps climbing.

Climate projections paint an even more concerning picture. The BGS estimates that just 3% of British properties faced significant subsidence risk in 1990. By 2070, that figure is expected to reach 10%—more than triple. In London specifically, claim volumes are projected to rise by 57% over the same period.

This isn’t a problem for future generations to worry about. It’s happening now, and homeowners need to understand what they’re dealing with.

What Causes Subsidence in British Properties

Unlike California, where subsidence primarily results from extracting groundwater from deep aquifers, UK subsidence stems from a different set of factors—ones that hit closer to home, quite literally.

Clay Shrink-Swell — The Southeast’s Hidden Enemy

If your property sits on London Clay, you’re living on one of the most reactive soil types in the country.

Clay soils behave almost like a sponge. When they absorb water during wet weather, they swell. When they dry out in summer, they shrink—sometimes dramatically. This constant expansion and contraction is called clay shrink-swell, and it’s responsible for the majority of subsidence damage in the UK.

The problem is most severe in London and the Southeast, where London Clay underlies vast swathes of residential property. This particular clay formation is among the most shrinkable in Britain, highly sensitive to moisture changes that can shift your foundations with the seasons.

In a normal year, this seasonal movement goes largely unnoticed. Your house shifts slightly in summer, settles back in winter, and life carries on. The trouble starts during extended dry spells—like the heatwaves of 2018, 2022, and 2025—when the soil stays contracted through what should be wetter months, then shrinks even further when summer returns.

That’s when cracks appear. And once they do, the damage has already begun.

For property owners concerned about ground stability in urban environments, understanding how modern smart city monitoring technologies can track these changes is increasingly important.

Trees and Vegetation — The 60% Factor

Here’s a statistic that surprises many homeowners: trees and vegetation are implicated in more than 60% of subsidence claims in the UK.

It’s not that trees are inherently problematic. The issue is what happens when moisture-hungry species grow too close to buildings on clay soil. A mature oak tree can extract up to 1,000 litres of water from the ground every day during summer. When that extraction happens near your foundations, it accelerates soil shrinkage directly beneath your house.

Certain species pose greater risks than others. Willow, oak, poplar, and plane trees are particularly thirsty. The general rule of thumb: if a tree is within a distance equal to its mature height from your building, it could potentially affect your foundations.

This creates a genuine dilemma for many homeowners. That beautiful mature tree in your garden might be contributing to subsidence—but removing it isn’t straightforward. Tree Preservation Orders may prevent cutting. And paradoxically, removing a large tree on clay soil can trigger the opposite problem: heave, where the soil swells as it rehydrates, pushing your foundations upward.

It’s a situation where professional advice isn’t optional—it’s essential.

Leaking Drains and Broken Pipes

While clay shrinkage gets most of the attention, water can cause subsidence too—just through a different mechanism.

Leaking underground drains and broken pipes allow water to seep into the soil beneath your foundations. Over time, this water erodes and washes away fine soil particles, creating voids that your foundations can sink into. Unlike clay shrinkage, this type of subsidence can happen on any soil type.

The challenge is detection. A leaking drain often shows no obvious signs at surface level. The first indication might be subsidence damage to your property—by which point the underlying problem has been developing for months or years.

Historic Mining — The Legacy Beneath Your Feet

Step away from London and the Southeast, and subsidence takes on a different character entirely.

In Yorkshire, the Midlands, South Wales, and parts of the Northeast, historic coal mining has left a hidden legacy beneath thousands of properties. Old mine workings, abandoned shafts, and collapsed tunnels can cause the ground to shift decades after mining ceased.

The Coal Authority maintains records of past mining activity, and CON29M mining searches are a standard part of conveyancing in affected areas. But not all historic workings are documented—some date back centuries and were never properly recorded.

Mining-related subsidence operates under different rules than clay shrinkage. If your property damage results from coal mining, your claim goes through the Coal Authority rather than your home insurance. Understanding which type of subsidence you’re dealing with matters enormously for how you pursue remediation.

For those dealing with construction projects in areas affected by historic mining or unstable ground, professional ground deformation monitoring provides the kind of ongoing surveillance that traditional surveys simply can’t match.

UK Subsidence Risk: Understanding the Causes by Region

🏛️ London & Southeast

Primary cause: Clay shrink-swell

Key factor: London Clay + mature trees

Risk level: 1 in 50 properties affected

⛏️ Yorkshire, Midlands & Wales

Primary cause: Historic coal mining

Key factor: Collapsed workings & shafts

Risk level: Variable by specific location

🏠 Nationwide Risk Factors

Leaking drains: Any soil type

Shallow foundations: Pre-1976 builds

Climate change: Increasing all risks

Source: British Geological Survey GeoSure datasets and ABI claims data

Which Properties Are Most at Risk

Not all homes face equal subsidence risk. Certain combinations of age, construction, and location create perfect conditions for ground movement problems.

Victorian and Edwardian Homes — Beautiful but Vulnerable

If you own a Victorian or Edwardian property, particularly in North London or the Southeast, you’re sitting on a higher-risk combination.

The issue isn’t the quality of construction—these homes were built to last, and many have stood for well over a century. The problem is foundation depth. Building regulations of the era didn’t require deep footings. Many Victorian and Edwardian houses were constructed with shallow foundations sitting directly on the upper layers of soil, where moisture changes are most dramatic.

Modern building regulations, significantly updated after the 1976 drought, require foundations deep enough to avoid the zone where seasonal shrinkage and swelling occurs. Properties built before these changes—essentially anything pre-1976—don’t have that protection.

Bay windows present a particular vulnerability. These architectural features, so characteristic of period properties, often rest on even shallower foundations than the main structure. They’re frequently the first part of a building to show subsidence damage.

The numbers bear this out: an estimated one in 50 houses in London and the Southeast has suffered from subsidence at some point. In areas of North London where Victorian terraces sit on London Clay with mature street trees nearby, that ratio is even higher.

The Climate Change Escalator

What’s particularly concerning is that subsidence risk isn’t static—it’s accelerating.

BGS modelling shows that climate change will significantly increase clay-related subsidence pressures over coming decades. The mechanism is straightforward: hotter, drier summers mean more soil shrinkage. Wetter winters mean more swelling. More extreme cycles mean more damage.

The projections are sobering. Properties facing high subsidence risk are expected to rise from around 3% of British housing stock in 1990 to over 10% by 2070. That’s not a gradual increase—it’s a fundamental shift in how many homeowners will need to think about ground stability.

More immediately, 2025 is shaping up as what insurers call a «surge year»—a period when subsidence claims spike dramatically above average. The UK experienced its warmest spring on record, following patterns similar to the surge years of 2018 and 2022. If you’ve noticed new cracks appearing this year, you’re not alone.

The True Cost of Subsidence for UK Property Owners

Understanding subsidence isn’t just about protecting your home—it’s about protecting your finances. The costs can be substantial, and they extend far beyond the repair bill.

Insurance Claims and the £17,000 Average

When subsidence strikes, home insurance is typically your first line of defence. Most buildings policies cover subsidence as a named peril, though terms, excesses, and exclusions vary.

The standard excess for subsidence claims is £1,000—significantly higher than for other types of damage. And the average payout tells its own story: £17,264 as of early 2025, up from around £10,000 just three years earlier.

Why the increase? Partly inflation, partly complexity. Subsidence repairs often involve extended timelines, with insurers requiring monitoring over at least one full seasonal cycle before authorising permanent repairs. That means months of living with the problem before resolution begins.

The type of repair matters enormously for cost. Cases requiring underpinning—extending foundations deeper into stable ground—typically cost four to five times more than cases resolved through tree management or drain repair. With a growing preference for preserving trees (driven by environmental concerns and Tree Preservation Orders), more cases are heading toward expensive structural solutions.

Property Value — The 20% Drop Nobody Talks About

Beyond immediate repair costs, subsidence carries a longer-term financial sting: property devaluation.

A history of subsidence can reduce a property’s value by up to 20%. Even after repairs are complete and a Certificate of Structural Adequacy is issued, the stigma lingers. Future buyers will see the claim history in conveyancing searches. Future insurers will note it in their records.

Getting a mortgage on a property with subsidence history can be challenging. Getting insurance can be harder still—and more expensive. Some insurers simply decline to cover properties with previous claims, forcing owners into specialist markets with premium pricing.

This creates a painful dynamic for many homeowners. You might suspect early subsidence, but hesitate to make a claim because of the long-term implications for your property’s marketability. It’s an understandable concern—but delaying action typically makes the eventual outcome worse, not better.

The Hidden Costs Beyond Repairs

The headline repair figure rarely captures the full financial impact of subsidence.

Consider the monitoring period: insurers typically require evidence that movement has stabilised before authorising permanent repairs. That can mean 12 to 18 months of living with cracks, sticking doors, and the stress of uncertainty. If movement continues, the timeline extends further.

Professional fees add up quickly. Structural engineer assessments, CCTV drain surveys, arboricultural reports, ongoing crack monitoring—each comes with its own invoice. Even if insurance covers the eventual repair, many of these preliminary costs fall on the homeowner.

Then there’s the less quantifiable toll: the stress of living in a home you’re not sure is stable, the disruption of repair works when they finally happen, and the nagging worry about what this means for your family’s largest asset.

The Real Cost of Subsidence: What Homeowners Face

💷 Direct Costs

- Average insurance claim: £17,264

- Standard excess: £1,000

- Underpinning (if needed): £10,000–£50,000+

- Tree removal/root barrier: £500–£3,000

- Drain repair: £500–£3,000

- Structural engineer report: £400–£1,000

📉 Long-Term Impact

- Property devaluation: up to 20%

- Higher insurance premiums post-claim

- Difficulty obtaining future mortgages

- Disclosure requirements when selling

- Potential buyer reluctance

- Reduced negotiating position

✅ The Prevention Alternative

Satellite monitoring costs a fraction of repair expenses and can detect movement before damage occurs—potentially avoiding claims entirely and preserving your property’s value and insurability.

Protect Your Property Portfolio

For landlords and property investors managing multiple assets, satellite monitoring offers portfolio-wide risk assessment at a fraction of individual survey costs. Identify which properties need attention before problems escalate.

Discuss Your Portfolio →SkyIntelGroup delivers institutional-grade ground monitoring for private investors.

How to Spot Subsidence Warning Signs

Knowing what to look for can help you catch subsidence early—though as we’ll see, visible signs often mean the problem is already well established.

The Crack Code — What Different Patterns Mean

Not every crack signals subsidence. Houses move and settle naturally, thermal expansion creates stress, and plaster can crack for reasons entirely unrelated to ground movement. Learning to read cracks helps distinguish the concerning from the cosmetic.

Subsidence cracks typically share several characteristics. They’re diagonal, running at an angle rather than horizontally or vertically. They’re tapered—wider at one end than the other. And crucially, they’re wider at the top than at the bottom, reflecting the way the building rotates as one side sinks.

The width matters too. The Building Research Establishment classifies cracks by severity. Hairline cracks under 1mm are generally cosmetic. Cracks between 1mm and 5mm warrant monitoring. Anything over 5mm—roughly the thickness of a pencil—indicates significant movement requiring professional investigation.

Location provides clues as well. Cracks radiating from window and door corners are classic subsidence indicators, as these are natural stress concentration points. Cracks that appear both inside and outside the property, aligned through the wall, are more concerning than surface-only cracking.

Beyond Cracks — Other Red Flags

Subsidence doesn’t always announce itself through wall cracks alone. Several other symptoms can indicate ground movement:

Doors and windows sticking without obvious cause—particularly if they worked fine previously and multiple openings are affected simultaneously. Seasonal sticking related to humidity is normal; sudden onset across multiple frames is not.

Wallpaper rippling or tearing at joints, especially in corners where walls meet ceilings. This can indicate the building is distorting as foundations shift.

Gaps appearing between skirting boards and floors, or between walls and ceilings. Any sign that previously flush surfaces are separating deserves attention.

Uneven or sloping floors that develop over time rather than being original features of the building.

When to Call a Professional

If you notice Category 2 or higher cracks (over 1mm), or multiple warning signs appearing together, professional assessment is warranted.

A RICS-qualified surveyor can conduct a thorough inspection, measuring and documenting cracks, assessing their pattern and severity, and forming a view on likely causes. For significant concerns, a structural engineer’s report provides more detailed technical analysis.

Many homeowners start by monitoring cracks themselves—marking their ends with pencil, measuring widths with a crack gauge or ruler, and photographing them monthly with a scale reference. This creates valuable documentation if the situation escalates, and helps distinguish active movement from historic, stable cracks.

But here’s the limitation of all these approaches: they’re reactive. By the time cracks are visible enough to measure, damage has already occurred. The question is whether there’s a better way.

Why Traditional Detection Methods Fall Short

The conventional approach to subsidence follows a predictable pattern: notice damage, report to insurer, wait for assessment, monitor for a season, address the cause, then repair. It works, eventually—but it has significant drawbacks.

The Waiting Game Problem

Insurance companies require evidence that movement has stabilised before authorising permanent repairs. That typically means monitoring through at least one complete seasonal cycle—watching crack gauges through summer shrinkage and winter recovery.

This makes sense from an underwriting perspective. Repairing a building that’s still moving wastes money. But for homeowners, it means months of living in limbo, watching cracks and hoping they stop growing.

During that time, damage may continue accumulating. What started as a cosmetic issue can progress to structural concern. And the stress of uncertainty takes its own toll.

Point Measurements vs. Area Coverage

Traditional crack monitoring measures specific points: this crack, that doorframe, those gauge locations. It tells you what’s happening at those exact spots, but nothing about the broader picture.

What if the most significant movement is occurring where you haven’t placed a gauge? What if the crack you’re monitoring is a symptom of deeper issues that aren’t yet visible? Point measurements can’t answer these questions.

Building surveys provide a snapshot—conditions at one moment in time. They’re valuable for assessment, but they don’t show trends. Is movement accelerating, stabilising, or already stopped? A single survey can’t tell you.

The Missing Piece — What’s Happening Under the Surface

Here’s the fundamental challenge: visible damage is a lagging indicator. By the time you can see cracks, the ground has already moved enough to stress the structure. By the time cracks are wide enough to measure confidently, movement may have been occurring for months or years.

What homeowners and professionals really need is a leading indicator—something that detects ground movement before it translates into building damage. Something that covers whole areas rather than individual points. Something that tracks change over time rather than capturing isolated snapshots.

That technology exists. And it’s been watching from space.

How Satellite Technology Detects Subsidence Before Damage Appears

The most significant advance in subsidence detection doesn’t involve engineers on the ground at all. It comes from satellites orbiting hundreds of kilometres overhead.

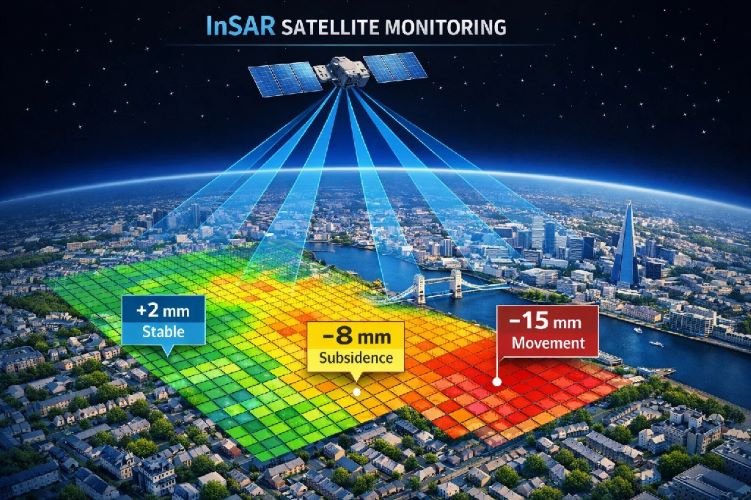

InSAR Monitoring — Millimetre Precision from Space

InSAR—Interferometric Synthetic Aperture Radar—represents a fundamental shift in how we can monitor ground movement.

The concept, stripped of jargon, is straightforward. Satellites equipped with radar sensors orbit the Earth, bouncing signals off the ground and measuring how long they take to return. By comparing measurements from multiple passes over the same area, analysts can calculate precisely how much the surface has moved between observations.

The precision is remarkable: modern InSAR technology detects movement as small as a few millimetres. That’s far more sensitive than any crack gauge, and it measures actual ground movement rather than its structural consequences.

Even more valuable is the coverage. A single satellite pass can monitor an entire city, identifying movement patterns across thousands of properties simultaneously. Instead of measuring a few points and hoping they’re representative, you’re seeing the complete picture.

How Leading Organisations Already Use Satellite Data

This isn’t experimental technology—it’s already mainstream among those who deal with subsidence professionally.

The British Geological Survey incorporates satellite monitoring into their GeoSure hazard datasets. Major insurers use it for portfolio risk assessment and claims verification. Property data companies like Groundsure now include weekly satellite movement data in their GeoRisk reports, providing surveyors with objective evidence of building movement.

The reason is simple: satellite data provides something that traditional methods can’t. It shows actual movement, measured independently, across whole areas, tracked over time. When a surveyor reports that a building shows signs of historic subsidence, satellite data can confirm whether movement is genuinely historic or quietly continuing.

From Reactive to Proactive — The Detection Revolution

The transformative potential of satellite monitoring lies in shifting from reactive to proactive management.

Traditional approach: wait for damage, then respond. Satellite approach: detect movement early, then intervene before damage occurs.

Because satellite archives extend back years, analysts can establish historical baselines for any property. How has the ground beneath your house behaved over the past decade? Is there a pattern of seasonal movement? Any long-term trend?

This context transforms decision-making. A property buyer can see objective movement history before purchasing. A homeowner noticing early warning signs can verify whether they correlate with actual ground movement. A landlord managing a portfolio can identify which properties warrant attention and which are stable.

The technology that governments and corporations have used for years is now accessible to individual property owners. And in a climate where subsidence risk is accelerating, that accessibility matters more than ever.

Who Benefits from Satellite Subsidence Monitoring in the UK

While the technology serves anyone concerned about ground stability, certain groups find particular value in satellite monitoring capabilities.

Homeowners and Property Buyers

For individual homeowners, satellite monitoring answers questions that traditional surveys can’t.

Before buying a property: Conveyancing searches reveal whether a property has a claims history, but they don’t show current stability. Satellite data can reveal whether the ground is actively moving, providing crucial due diligence information that complements standard surveys.

When you notice warning signs: Those hairline cracks could be nothing—or they could be early indicators of a developing problem. Satellite monitoring can confirm whether actual ground movement correlates with your observations, helping you decide whether to escalate concerns or rest easy.

For peace of mind in high-risk areas: If you live on London Clay near mature trees, you know you’re in a higher-risk category. Ongoing monitoring provides early warning if conditions change, rather than waiting for damage to appear.

To support insurance claims: When you do need to make a claim, objective satellite data documenting ground movement strengthens your case and can help resolve disputes about causation.

Property Investors and Landlords

For those managing property portfolios, satellite monitoring offers efficiency that individual surveys can’t match.

Portfolio-wide risk assessment: Identify which properties in your portfolio sit on moving ground and which are stable. Prioritise inspection and maintenance spending where it’s actually needed.

Pre-acquisition due diligence: Before adding a property to your portfolio, understand its ground stability history. Make informed investment decisions based on objective data.

Tenant safety and compliance: Demonstrate proactive management of property risks. Document that you’re monitoring ground stability across your holdings.

Asset value protection: Catch problems early, before they escalate into expensive repairs and damaging claims history.

Surveyors and Conveyancing Professionals

For property professionals, satellite data enhances service quality and reduces risk.

Objective evidence: Back up visual inspection findings with independent movement data. When you report signs of historic subsidence, satellite records can confirm the timeline.

Enhanced due diligence: Offer clients a more comprehensive picture than visual inspection alone provides. Differentiate your service in a competitive market.

Professional liability protection: Document that your assessments incorporated all available data sources. Demonstrate thorough methodology if findings are later questioned.

Insurance Companies

Insurers increasingly recognise satellite monitoring as a valuable tool for managing subsidence exposure.

Underwriting risk assessment: Evaluate property-specific subsidence risk before setting terms, rather than relying solely on postcode-level data.

Claims verification: When claims are filed, satellite data provides independent evidence of ground movement patterns, helping verify genuine claims and identify anomalies.

Portfolio exposure analysis: Understand aggregate subsidence risk across policy portfolios, particularly heading into potential surge years.

Who Uses Satellite Subsidence Monitoring?

Homeowners

Pre-purchase checks, early warning, claims support

Property Investors

Portfolio screening, acquisition due diligence, asset protection

Surveyors

Enhanced reports, objective evidence, service differentiation

Insurers

Risk assessment, claims verification, portfolio analysis

How SkyIntelGroup Delivers Subsidence Intelligence

At SkyIntelGroup, we specialise in translating satellite data into actionable intelligence for property owners and professionals. Our team brings together expertise in remote sensing, geospatial analysis, and practical property risk assessment.

What We Deliver

Every engagement is tailored to your specific needs, but our core deliverables include:

Deformation maps showing ground movement across your area of interest. Colour-coded visualisations make it immediately clear which zones are stable and which show movement—no technical background required to understand the results.

Historical baseline analysis drawing on years of archived satellite data. We establish how the ground beneath your property has behaved over time, revealing any long-term trends that might not be apparent from recent observations alone.

Time-series tracking that shows movement evolution month by month, quarter by quarter. This longitudinal view distinguishes seasonal fluctuations from genuine subsidence trends.

Risk assessment reports that synthesise our findings into clear, practical conclusions. We don’t just provide data—we tell you what it means for your property and what, if anything, you should consider doing.

GIS-compatible outputs for professionals who need to integrate our findings with other geospatial information. Our data works seamlessly with standard mapping and analysis platforms.

How Our Process Works

Working with us follows a straightforward path:

Initial consultation: We discuss your situation, understand your concerns, and determine what analysis will best serve your needs. This might be a one-time assessment or an ongoing monitoring arrangement.

Scope definition: We define the area of interest—whether a single property, a portfolio of holdings, or a development site—and confirm the timeframe for historical analysis.

Analysis and delivery: Our team processes the satellite data, performs the technical analysis, and prepares your deliverables. Turnaround depends on scope, but we prioritise efficiency without compromising thoroughness.

Interpretation support: We don’t just hand over data and walk away. We explain what we’ve found, answer your questions, and help you understand implications for your specific situation.

For ongoing monitoring needs, we establish regular reporting cycles—quarterly or annually depending on risk level and your preferences—providing continuous visibility into ground stability.

Our Process: From Enquiry to Intelligence

Consultation

Understand your needs and define the right approach

Analysis

Process satellite data and establish movement patterns

Delivery

Clear reports with visualisations and practical conclusions

Support

Interpretation guidance and ongoing monitoring options

Find Out What’s Happening Beneath Your Property

Whether you’re concerned about a specific property, evaluating an acquisition, or managing a portfolio, we can show you the ground truth—literally. Get in touch to discuss how satellite monitoring can help.

Request Your Assessment →Free initial consultation • No obligation • Results you can act on

Frequently Asked Questions

How common is subsidence in the UK?

Subsidence affects a significant number of British properties, though risk varies dramatically by location. In London and the Southeast, approximately one in 50 homes has experienced subsidence at some point. Nationally, insurers handled around 45,000 domestic subsidence claims in 2024—a figure that rises sharply after hot, dry summers. The British Geological Survey projects that subsidence risk will affect roughly 10% of British properties by 2070, up from around 3% in 1990, driven primarily by climate change intensifying the shrink-swell cycle in clay soils.

Will my insurance cover subsidence damage?

Most standard buildings insurance policies cover subsidence as a named peril, subject to terms and conditions. The typical excess for subsidence claims is £1,000—higher than for other types of damage. However, coverage isn’t automatic: policies may exclude properties with previous subsidence history, or apply special conditions in high-risk areas. After making a claim, you may find renewal terms change or premiums increase. If subsidence results from coal mining rather than natural causes, compensation comes through the Coal Authority rather than your home insurer. Always check your specific policy wording and disclose any concerns promptly.

Can subsidence be fixed permanently?

Yes, but the approach depends on the cause. If tree roots are the culprit, solutions range from removing the tree to installing root barriers—though tree removal on clay soil must be managed carefully to avoid triggering heave. Leaking drains require repair or replacement. For cases where the cause can’t be eliminated or movement is severe, underpinning extends foundations into more stable ground, providing a permanent structural solution. Modern techniques like resin injection offer less invasive alternatives to traditional mass concrete underpinning. The key is correctly identifying and addressing the root cause; repairing cracks without fixing the underlying problem simply means they’ll return.

How accurate is satellite monitoring compared to traditional surveys?

Satellite InSAR monitoring detects ground movement with millimetre-level precision—more sensitive than visual observation or standard crack gauges can achieve. More importantly, it measures actual ground movement rather than its structural consequences, providing earlier warning than waiting for visible damage. The technology covers entire areas rather than individual points, revealing patterns that spot measurements might miss. Major organisations including the British Geological Survey, property data companies, and insurers already incorporate satellite monitoring into their assessments. The limitation is that InSAR measures surface movement; it doesn’t directly diagnose causes, which is where it complements rather than replaces professional structural assessment.

Is my Victorian home at higher risk?

Victorian properties do face elevated subsidence risk, particularly in London and the Southeast. The primary factor is foundation depth: buildings constructed before modern building regulations (significantly updated in 1976) typically have shallower foundations that sit within the zone where soil moisture changes most dramatically. When this combines with shrinkable clay soil and proximity to moisture-hungry trees, risk increases substantially. Bay windows, a characteristic Victorian feature, often rest on even shallower foundations than the main structure. However, Victorian construction also tends to be relatively tolerant of movement thanks to flexible lime mortar. Risk depends on multiple factors—soil type, nearby vegetation, drainage condition—not just age alone.

Protect Your Property Before the Next Heatwave

The UK’s subsidence problem isn’t going away. Climate change is making hot, dry summers more frequent and more intense. The shrink-swell cycle that drives most British subsidence is accelerating. And millions more properties are expected to face significant risk in the coming decades.

But knowledge is power. Understanding what causes subsidence, recognising warning signs, and knowing your property’s ground stability history puts you in control rather than at the mercy of circumstances.

Traditional approaches—waiting for damage, then reacting—will always have a place. But satellite technology now offers something better: the ability to see ground movement before it becomes building damage, to make informed decisions based on objective data, and to act proactively rather than reactively.

Whether you’re a homeowner who’s noticed some concerning cracks, a buyer considering a period property in a high-risk area, an investor managing a portfolio, or a professional advising clients on property risk—ground truth matters. And it’s never been more accessible.

The next surge year is always closer than it seems. The time to understand your property’s ground stability is before you need to, not after the damage appears.